Industry regulators are nudging financial services companies to implement stricter regulatory controls and undertake modernization in compliance aspects of their businesses. Despite detailed guidelines and extended compliance timeframes, many organizations struggle and lag in following these. According to a study by S&P Global Market Research, partnerships between banks and fintech companies that offer banking as a service will be subject to greater scrutiny and will need to prioritize regulatory compliance starting in 2023. In an industry replete with regulations, businesses are embracing technology to strengthen their compliance management and minimize any gaps from a regulatory perspective.

Technology continues to alleviate several industries from the limitations posed by legacy systems, and is now sweeping through financial institutions. Regulatory Technology (RegTech) is emerging as a powerful subdomain of the Fintech ecosystem, helping organizations close the compliance gap and reduce costs associated with it, while maintaining a superior customer experience. Leveraging RegTech to assist with these challenges is expected to be the key factor differentiating adaptive organizations from those failing to keep pace with dynamism.

What is RegTech?

Put simply, RegTech can be defined as “the use of new technologies to solve regulatory and compliance requirements more effectively and efficiently.”

–Institute of International Finance

RegTech is a branch of fintech that deploys sophisticated technological solutions comprising artificial intelligence, big data, and machine learning, among others, to navigate the increasingly dense data landscape and automate compliance processes with an aim of making them more efficient and cost-effective. It is designed to enable organizations to keep up with the constantly evolving regulatory and governance landscape.

The deployment of technology to bridge regulatory and operational gaps is not a new concept for organizations. What, then, is different and unique about RegTech? While FinTech improves and automates financial services such as payment systems, lending platforms, and collections processes, RegTech enables adherence to regulatory requirements and governance protocols in particular through the deployment of multifaceted technological capabilities. Its key characteristics include the following:

- Speed: Creating reports is quick and simple to configure.

- Agility: Interconnected and cluttered data sets can be separated and organized.

- Integration: Solutions are implemented much more quickly.

- Analysis: RegTech is able to fully realize the potential of vast “big data” repositories by skillfully extracting insightful knowledge from them.

Challenges faced by financial institutions facilitate the need for RegTech

Since the 2008 global financial crisis, an increasing number of regulations have made their way into the financial services industry. The environment has become more complicated after multiple economic crises and uncertainties that have continued to plague the global economy thereafter. To equip businesses to handle such uncertainties, governments have made frequent changes to expand the scope of financial regulations. Organizations have to incur high overhead costs for the production and deployment of solutions to comply with the modifications to existing regulations. Large penalties are levied in response to any noncompliance that occurs. As an example, the Government of India released the Digital Personal Data Protection Bill (DPDP Bill), in November, 2022, to implement stricter controls over the privacy of digitized personal data. The Bill imposes penalties up to INR 500 crores per instance, for non-compliance in this specific area alone.

Additionally, legacy systems pose the challenge of limited automation and lack of digital transparency to meet the pace of regulatory changes. Insufficient integration, non-compatibility of systems, and a non-standardized approach are additional roadblocks.

Since the complexity of these challenges is expected to increase further, financial institutions are stepping back to evaluate manual processes and achieve automation to reduce regulatory risk and achieve sound financial health. Through digitization, RegTech gives businesses the ability to create cost-effective solutions to withstand regulatory challenges. On the other hand, RegTech strengthens the regulators supervisory capacity by leveraging unified formats for monitoring the dynamic advancements in the financial sector.

Technologies in RegTech and how they contribute to its development

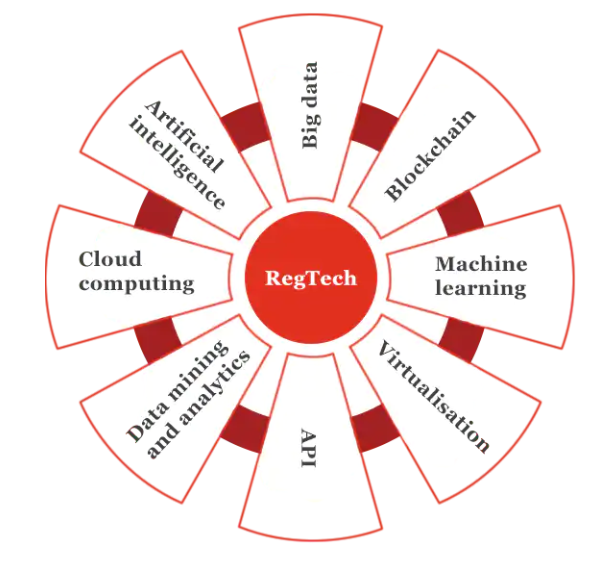

Financial institutions are developing robust compliance protocols by leveraging FinTech solutions with RegTech innovation. Operating on various business models and complex legal structures, metrics, and risks, they are strengthening internal control mechanisms, compliance assessment, and procedural management. The various intervention areas that RegTech has used to help financial institutions are summarized below.

Source: PwC India

As the image shows, RegTech utilizes Artificial Intelligence, Machine Learning, APIs, Image Virtualization, Cloud Computing, Big Data, Analytics, and Blockchain, in addition to other derivatives of these capabilities. The following section discusses a few of the innovations that were developed as a result and are improving financial institutions’ efficiency.

- Visual analytics: The finance function is facing new challenges, and leaders are grappling with vast and diverse data sets. As such, there is a need to set new benchmarks for accuracy and quality of reporting. Shifting away from deploying human capital for regular tasks, FIs are turning to visual analytics tools for data-driven business insights. Leveraging business rules, visual analytics tools measure a wide array of information, including profitability, efficiency, growth, capital, and funding. They can assess metrics like return on investment, efficiency ratio, revenue growth, Risk Weighted Assets (RWA), and Liquidity Coverage Ratio (LCR). Additionally, these tools possess the capability to conduct trend analysis, sensitivity analysis, scenario analysis, anomaly detection, early warning, and predictive modeling across various timeframes.

- Report automation platforms: Numerous banks have adopted report automation tools to reduce reporting errors and enhance efficiency. These tools offer an automated approach to gathering data, consolidating balances, and generating regulatory reports using an intuitive interface. Automation tools come with a wide range of capabilities, ranging from basic report submission and edit checks to more advanced functionalities like data sourcing, aggregation, and mapping. For global organizations, many report automation tools provide the advantage of a centralized platform to consolidate and produce regional reports efficiently.

- Robotics, or Robotic Process Automation: Robotic Process Automation (RPA) employs software to execute business processes in a controlled and repetitive manner. This automation enables financial services organizations to automate high-volume, computer-based tasks, mimicking the actions of human business users. The IT and operations teams oversee the continuous operation of these software-enabled robots, which coexist with the current IT infrastructure.

Robotics tools enable users to free up time for analysis by displacing manual processes in the world of RegTech. Moreover, when combined with other automation technologies like AI and ML, RPA further enhances efficiency, creating a primarily virtual workforce capable of executing tasks, communicating, learning from data sets, and even making decisions.

Financial services organizations have already embraced robotics in various functions, particularly those involving heavy transaction volumes. This includes tasks like routine compliance monitoring, testing, identifying discrepancies, and automating manual regulatory reporting processes. Forward-thinking Internal Audit (IA) departments within these organizations are exploring opportunities to shift manual, repetitive tasks to technology-enabled robots to elevate their testing processes.

- Business Process Management: Amidst the current economic climate, organizations are actively seeking cost efficiencies across all departments. To achieve this goal, many are turning to Business Process Management (BPM) as a systematic approach to enhance the effectiveness, efficiency, and adaptability of their processes in the face of a constantly changing environment. BPM encompasses a set of methods, tools, and technologies used to design, implement, analyze, and control operational business processes.

The BPM market is anticipated to experience substantial growth, especially with the emergence of mobile cloud solutions that are shaping the BPM landscape. Globally, the BPM market is expected to grow at a compounded annual growth rate (CAGR) of 10.5%, reaching a size of USD 14.4 Billion by 2025.

Source: Statista 2023

BPM technology solutions offer comprehensive capabilities, enabling organizations to design, model, simulate, build, execute, monitor, and optimize their processes. These tools facilitate the easy identification of process improvements and the early detection of issues or defects within the processes.

RegTech and the ecosystem of debt collections

Fintech solutions have been a major catalyst for reshaping the debt collections industry. The practice of leveraging solutions powered by AI and ML is increasing to achieve cost efficiencies and a holistic customer experience. In an industry there is a lot of uncertainty on likely repayment defaults, the regulatory guidelines pertaining to debtor privacy and information security, and a constant need to keep NPLs minimal, lending institutions are certain to benefit from the application of RegTech. By embracing RegTech solutions with agile and open architecture, lenders can seamlessly integrate these tools into their existing systems. This approach significantly minimizes the need for costly and time-consuming updates. The flexibility of such RegTech solutions enables swift and smooth assimilation, allowing financial institutions to leverage their benefits without undergoing extensive overhauls.

If implemented correctly, one of the key outcomes of RegTech is process streamlining and cost efficiency. In a space where historically several interventions have been manual, lending institutions struggle to simplify end-to-end processes at low cost. From onboarding to debt resolution, automation can significantly reduce errors due to human biases, standardize data, and improve compliance and reporting capabilities. While human capital cannot be entirely replaced, lenders can focus on reallocating resources, analyze output, and apply critical judgment. This simplification of mechanisms will inevitably lead to a reduction in costs and a maximization of output for lending institutions.

Another key consideration in making debt collections effective and compliant is humanizing the processes and making decisions that are borrower-centric. The recovery of loans is a process that gradually moves away from being purely transactional, to being more empathetic and humane, thereby leading to borrower loyalty and better resolution rates. RegTech solutions such as risk assessment and onboarding tools can make touchpoints with borrowers more structured, leading to fewer grievances and complaints. The issue of data privacy can also be addressed by utilizing secure digital platforms (not email) for debtors to access their loan information in machine-readable formats. As a result, due diligence requirements can be met while ensuring successful engagement based on human-centric practices.

Compliance is a regular prerequisite at each stage of the debt collections process. With the growth of regulated and consolidated business establishments, unstructured or manual information recording can lead to business inconsistencies. Lenders can fully identify and evidence all of the risks associated with the recovery processes to the extent that the borrower information and terms of the debt are compliant and documented. We can anticipate that RegTech will promote standardization, increase transparency between lending institutions and regulators, and continue to benefit all stakeholders.

RegTech: A crucial and forward-looking requirement

In view of the dynamic economic landscape globally, it is unlikely that regulatory bodies will ease on issuing new compliance guidelines. As modern control mechanisms emerge, efforts to cut costs by switching to innovative technologies will get stronger. To comply with regulatory requirements, businesses will need to adopt transparency and create a structure around reporting and monitoring tasks.

RegTech will keep lenders in good standing as far as onboarding, engagement, and debt resolution are concerned in the debt collections landscape with an increased focus on borrower centricity. It is no exaggeration to say that regulators, RegTech organizations, lenders, and financial institutions will have to work together in an effort to continue innovation and revamp the regulatory environment in the global financial industry. Exploiting the transformative potential of RegTech will undoubtedly propel the financial industry into a future where leaders are uncompromising on compliance and empowered in their decision-making, transforming the way they safeguard businesses and serve customers.