The Indian Government and the RBI have been diligently working on introducing credit innovations to previously untapped segments, including those new to credit and the underserved rural population. Among these, agricultural loans have witnessed an increase, owing to factors such as prolonged monsoons and erratic rainfall patterns that impact crop production and yield. The Kisan Credit Card Scheme is a significant initiative aimed at helping farmers overcome financial challenges by providing them with access to quick and affordable credit.

As per a Statista report in FY 2022, Uttar Pradesh had over 10 million operative credit cards under the Kisan Credit Card scheme, followed by Maharashtra and Andhra Pradesh with 6.9 million and 6.2 million cards, respectively. The RBI is now spearheading efforts to digitize the issuance of Kisan Credit Cards, aiming to reduce the loan application processing time. In this article, we will explore the influence of technology on the disbursement and collections of Kisan Credit Card Scheme loans.

What is Kisan Credit Card (KCC)?

Indian banks launched the Kisan Credit Card (KCC) program in 1998 to issue Kisan Credit Card to farmers. With these cards, farmers can make cash withdrawals for their agricultural production needs as well as purchases of agricultural inputs like seeds, fertilizers, and pesticides. Several banks, including the State Bank of India, HDFC Bank, ICICI Bank, and Axis Bank, offer the Kisan Credit Card. The KCC scheme was established with the primary objective of rural financial inclusion by meeting the comprehensive credit requirements of the agriculture sector and providing essential financial support to farmers.

While many MFIs and NBFCs provide crop loans, obtaining new loans becomes a challenge for farmers with existing dues or default histories. This forces the farmers to resort to non-institutional sources for borrowing. Peer-to-peer platforms and requesting small amounts of cash from family members, particularly for pre-sowing, put farmers under stress and financial strain. The KCC is useful in situations like this.

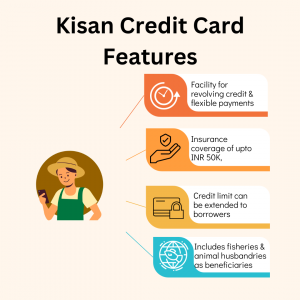

Fig: Features of Kisan Credit Card

What is the online process for Kisan Credit Card application?

PM Kisan beneficiaries can apply for KCC in online/ offline modes. The online process is as below:

Step 1: The applicant visits the online bank site for the Kisan credit card scheme

Step 2: Under the KCC scheme, the bank website will redirect to the application page.

Step 3: The applicant need to fill the form with the required details and click on ‘Submit’.

Step 4: On doing so, an application reference number will be sent.

Step 5: After eligibility verification, the bank will get back to the applicant for the further process within 3-4 working days.

Step 6: Once the requirements are complete, the loan officer at the bank can assist the applicant with the loan amount

Enhancing Kisan Credit Card Loan Disbursement with Technology

The pilot project focused on digitizing KCC lending has the potential to revolutionize the rural credit delivery system. During its initial phase, the RBI plans to create a frictionless card revolution, starting with Kisan Credit Card loans, dairy loans, and collateral-free MSME loans offered through the participating banks. The platform’s use will result in reducing operational costs, accelerating loan disbursement, and enhancing the scalability of KCC disbursals to eligible farmers, ultimately reducing the cost of borrowing for this segment. The platform can also incorporate services like Aadhaar e-KYC, land records from select state governments, and PAN validation, reducing the need for in-person visits to branch offices and complicated paperwork.

The platform creates opportunities for fintech and agritech companies to innovate and further streamline Kisan credit card loan disbursements.

Tech-Driven Collections as a Game Changer for KCC

Between 2001 and 2020, India experienced seven El Nino years, four of which resulted in droughts, leading to a decline in farm output and inflationary pressures. The chances of farmers defaulting on loan payments rise, and coercive actions for loan recovery aggravate the situation. Loan waivers offered to farmers also added pressure on banks in terms of non-performing assets (NPAs). The rural and agricultural sectors need a proactive approach to collections rather than a compensatory one. AI/ML models, weather analytics, and insights from previous productions can create a framework for a collections strategy tailored to the borrower’s risk.

The recent introduction of the ‘Kisan Rin’ digital platform by the agricultural ministry is a welcome innovation. This platform offers a comprehensive view of farmer data, loan disbursement details, interest subvention claims, and scheme utilization progress. It promotes seamless integration with banks, enabling more focused and integrated agriculture credit and collections.

Credgenics Collections Platform for Streamlined Rural Debt Recovery:

Credgenics, a SaaS-powered collections technology platform, provides a range of modules designed to simplify loan collections in rural areas. Rural India had more than 425 million internet users, a whopping 44% more than urban India, which had 295 million people using the internet regularly, according to a report by Nielsen.

The farmers can be reached through digital channels such as SMS and WhatsApp for payment reminders in the pre-delinquency stages. Multilingual voicebots and chatbots facilitate communication between farmers and collections teams, addressing their queries and clarifying the impact on credit scores in the event of defaults. These bots can also capture the intent to pay, helping the lenders frame the next steps in collections via field collections or legal collections.

Credgenics’ CG Collect mobile app for field debt collections allows for easy tracking of field visits and debt recovery, especially in rural areas. It offers automatic reconciliation for lenders and eliminates paperwork for collections agents. The newly launched UPI collect feature for CG Collect enables farmers to make payments with a single click, eliminating the need for bank visits, NEFT, or debit transactions to make their loan repayments.

The Easy Settle module identifies potential settlement cases, allowing borrowers to request settlements against their dues. For lenders, it acts as a tool for finding leads in the NPA pool so that collections agents can talk to borrowers who are ready to settle their debts.

In Conclusion:

It is rightly said that farmers are the backbone of the economy; hence, the Kisan Credit Card has been a vital innovation in terms of financial inclusion for farmers. Controlling card issuance, however, becomes difficult when there is a high risk of credit abuse and when consumers are unaware of the advantages of the products and other borrowing options. Nevertheless, technology is set to drive new innovations in the agricultural sector, transforming credit disbursements and integrating digital collections into the KCC collections journey, further improving sector demands and needs.

If you are looking to transform your debt collections strategy with the power of digital and data-powered insights, reach out to us to request an exploratory session at sales@credgenics.com or visit us at www.credgenics.com

FAQs

What are the benefits of the Kisan Credit Card?

The Kisan Credit Card serves as a valuable financial tool for farmers, offering them access to short-term loans to cover their farming expenses. It provides the cardholders with the advantage of interest rates ranging from a mere 2% to 7%. It serves as a catalyst for increasing the overall business of banks. The scheme simplifies the typically cumbersome paperwork and loan application process, leading to more streamlined approvals and KCC disbursements. The Kisan Credit Card Scheme benefits are extended to the beneficiaries of the PM Kisan Samman Nidhi Yojana, further expanding its positive impact.

Who is eligible for a Kisan Credit Card?

The KCC is available to all farmers, including land owners, tenant farmers, sharecroppers, oral lessees, individual or joint cultivators, SHGs (Self Help Groups), and joint liability groups. The individual applying for the KCC must be within the 18–75-year age bracket and be engaged in farming and other agri-related activities.

What are the documents needed for a Kisan Credit Card?

- For KCC applications, farmers must present the following documents:

Aadhaar Card - Proof of being an Indian Resident

- Land ownership documents

- PAN card

- Mobile number

- Passport-size photo