Digital banking is the process of carrying out financial transactions using electronic devices that are connected to the internet, such as computers, tablets, and mobile phones. Digital banking offers a wide range of benefits to both customers and banking institutions. Customers can experience convenient and efficient banking with features like 24/7 access to accounts, bill payments, fund transfers, foreign exchange transactions, deposit creation, and security trading. Banks profit from digital banking because it enables process automation and lowers operating expenses. To understand in greater detail about what is digital banking, let us look at some of the key aspects associated with it.

Features of digital banking

Digital banking has many characteristics, making it the preferred choice for many customers. Some of its key features include:

Access to online channels: Customers who use online banking have 24/7 access to their bank accounts and can conduct transactions online. In addition to executing regular transactions, customers can submit service requests, such as applications for cards and cheque books, account detail modifications, or even applications for loans and credit cards. Since online banking is made available through a mobile application or website, it is easy for customers to manage their finances anywhere, anytime.

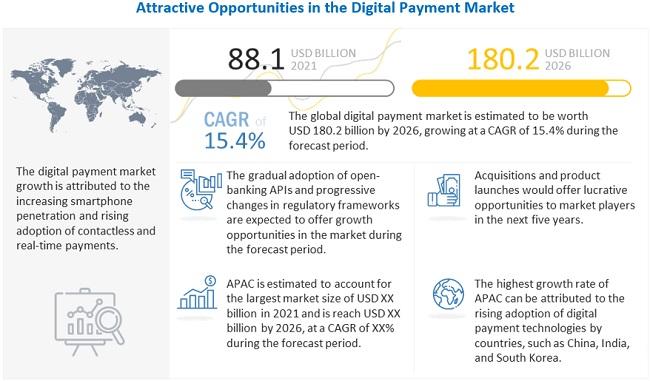

Digital wallets: Customers can store their credit and debit card information in a safe digital environment with the help of digital banking. The saved card details can then be used for online or in-store purchases. Digital wallets offer convenience and security, as customers are not required to carry their physical cards wherever they go. Owing to this ease of use, the global digital payment market is expected to rise at a CAGR of 15.4% by the end of 2026, per a report.

Source: MarketsandMarkets

Enhanced security: Digital banking offers advanced encryption technologies that protect customers’ data and transactions. Customers are also required to use multiple-factor authentication to access their accounts, which adds an extra layer of security.

How is digital banking useful to banks and their customers?

There are many ways in which digital banking is helpful to banks and their customers.

24*7 availability: Customers can access their accounts and other services as per their convenience. In cases of emergencies, where immediate funds are required, customers can execute transactions at the click of a button, irrespective of the time and their location.

User experience: Many banks offer rich online capabilities with many features. Banks offer personalized financial advice, savings schemes, purchase calculators, and even virtual assistants who help customers resolve various queries and make informed decisions. Some apps also offer spend analysis to give customers insight into the volume of different categories of expenditures.

A secure banking experience: Given the development of technology and the concurrent risk of fraud, security is the top priority for financial institutions. Although there are risks in the traditional banking setup, customers can experience digital banking in a much more secure way. Multiple-factor authentication makes it possible for users to have control over their accounts.

Source: Obopay

Digital banking services and the future

The experiences during the Covid-19 pandemic and other recent geo-political developments underlined the fact that in-person banking services can no longer be the only way forward. A hybrid model including digital banking, online and mobile banking, gives people more ways to access the financial services that are needed to manage their requirements. When banks create digital pathways that allow people to conduct their banking business remotely, it ensures that customer finances continue to grow, keeping up with the changes in how people conduct business.

Digital banking services have transformed the way the banking industry, and other industries supporting the banking sector operate. Mobile banking, remote deposits, digital wallets, digital payments, money transfers and other features give customers more autonomy regarding financial services. As technology advances, digital banking will become even more sophisticated and offer a wider range of benefits to customers and banks alike. The number of banking processes that are digitized is rapidly increasing, with end-to-end debt recovery mechanisms already transitioning. The rise in internet penetration and access to e-commerce, indicates the urgency for banks to make their digital platforms more robust and user-friendly, creating a win-win for customers and individual banking service platforms.

FAQs:

- Is digital banking secure?

The data is end-to-end encrypted so nobody other than the user and their bank can understand and read it while it is encrypted. The cipher strength is so strong that the hacker cannot break the code easily.

- What is digital banking’s impact on banks?

The main benefit of digital banking to banks is the significant reduction in operational costs. Automated processes eliminate redundant efforts and the costs arising thereof. It reduces the chances of error and enables efficiency in outcomes.

- Why is digital banking needed in India?

The biggest reason digital banking is a success in India is that it provides easy access to people living in remote locations who find it difficult to use physical bank branches and their banking services. While they may have no bank branch in their immediate vicinity, they can enjoy the benefits of banking if they have an internet-enabled mobile phone.

- What is the biggest challenge in digital banking?

The main challenge in digital banking is the sophistication of phishing attacks, due to which users unknowingly download malicious links and attachments on their systems, giving outsiders access to their confidential information.