With the growing prominence of digital banking across the global economic landscape, traditional banking processes are being challenged and transformed rapidly. Building on the advancements in technology and the emergence of innovative business models, it is possible to easily execute regular banking transactions online, through self-service channels and web-based applications. Customers now have access to digital wallets, instant payments, online money transfers, on-the-go investment opportunities, seamless foreign exchange transactions, and instant online purchases – all with the click of a button.

The modern electronic banking platform goes beyond being just a bank. It provides the most recent banking solutions in unique, secure, and customer friendly ways. In the post-demonetization landscape, digital banking emerged as the preferred choice for many customers. Standing in long queues to give paper-based instructions at retail banks became an avoidable exercise for many. The pandemic encouraged those who had previously felt disconnected from digital banking channels to adopt online banking as a new way of life. Going cashless and embracing remote banking are more important today, than ever. Like many other industries, the banking and financial services industry is being seen through the lens of automation and digitization.

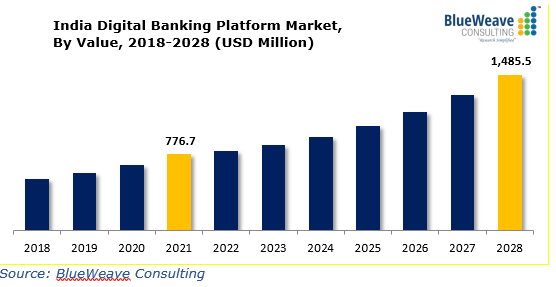

Source: BlueWeave consulting

There are many ways in which digital banking is benefiting customers, the banking industry, and the economy as a whole. Some of the benefits of digital banking are:

- Ease of transacting: One of the most significant benefits of digital banking is convenience for customers. The concept of ‘anytime, anywhere’ access resonates with customers across demographics. Owing to this convenience, the need to visit a physical bank has become redundant. Customers can access their accounts through smartphones or laptops from the comfort of their homes, offices or while on-the-go. Transferring funds, paying bills, checking account balances, and even placing requests for loans and credit cards is possible through digital channels. Those with aggressive schedules and less time on hand, prefer to transact with the ease that comes with digital banking, in comparison to standing in a long queue in a bank.

- Enhanced security: Digital banking offers heightened security compared to traditional banking methods. Multiple-factor authentication is a predominant security feature across many digital banking platforms. Users can set passwords, PINs, and biometric identification, to protect the account from unauthorized access. Additionally, most digital banking platforms offer real-time alerts to notify users of any suspicious activity on their accounts. This means that immediate action can be taken to prevent fraudulent transactions and protect finances.

- Lower cost: Since a lot of processes are automated, digital banking proves to be less expensive than traditional banking. Most banks offer lower fees and charges on digital platforms as compared to the transaction fees charged at brick-and-mortar branches, because they have lower overhead costs. This facilitates saving money on transaction fees, ATM fees and other bank charges. Additionally, many digital banks offer free or low-cost overdraft protection and no-fee checking accounts.

- The scope to go cash-free: Demonetization and the pandemic accelerated the adoption of cash-free transactions. This transition is inline with the Government of India’s agenda of making India a cash-less economy, enhancing digital financial literacy and doing away with the risks associated with excessive use of paper money. Digital banking is a major enabler to India’s burgeoning digital society. The popularity of UPI, mobile wallets, and internet banking allow users to make online purchases and sales, saving huge costs in the process. As per a report, over 72 billion digital transactions were recorded in the country in FY2022.

Source: Press Information Bureau

- Better financial management: Digital banking offers a range of tools and resources to enable effective management of finances. Financial calculators, budgeting tools, and other resources help customers track their expenditures and savings. It is also possible to manage liquid money better, set financial goals, and make well-informed decisions about one’s finances.

- Faster transactions: Execution of transactions is much faster on digital platforms than in traditional modes. This means there is no waiting period before transactions get settled or cleared, unlike traditional banking methods. Customers can transfer funds between different accounts, create fixed deposit accounts, access demat accounts, and place a variety of service requests with just a few clicks.

- 24*7 banking: While earlier banks used to operate for a fixed number of hours a day, for a few days a week, digital banking offers the flexibility of anytime banking. The challenge of not being able to visit a bank within a limited number of free hours is completely done away with because of the availability of digital banking services.

- Accessibility in remote locations: Perhaps one of the most crucial advantages of digital banking in India is that it allows people in remote locations to access banking services. Not every town or city may be in close proximity to a retail banking branch. Nevertheless, people living in such areas can open a bank account and carry out other banking activities through digital platforms. Digital banking is a definitive path toward financial inclusion and extending economic stability amongst the underserved and underbanked in our country.

While digital banking still has a long way to go before it becomes the mainstay operationally, it is safe to say that it offers tremendous flexibility and potential that will benefit the country’s banking sector. The benefits of digital banking are all-encompassing, including a superior customer experience, and unlocks the path for inclusive economic growth and stability. With a sizable portion of India’s population becoming aware of financial discipline and adept at digital platforms, the banking industry’s adoption of digital is becoming inevitable. Credgenics, India’s leading SaaS-based debt resolution and collections technology platform, offers banks and other non-banking lending companies the technological expertise to help transition debt collection services for the digital era. The acceptance of online end-to-end debt recovery processes is a stark departure from the traditional offline mechanisms previously deployed by the industry.

FAQs:

- What aspects of digital banking affect customers in India?

Customers using digital banking are influenced by several factors. The most important ones are convenience, speed of execution, security, connectivity in areas not having physical branches, and self-service benefits. These factors have been the major drivers for the adoption of digital banking in India.

- How safe is digital banking in India?

Digital banking has become popular in recent years, and its safety is one of the major reasons for the same. The Reserve Bank of India has implemented measures to ensure safety of digital banking transactions. These include multi-factor authentication across the banking sector for accessing self-service mobile applications and internet banking platforms. Additionally, customers can set transaction limits and receive real-time alerts for all transactions. In case of any unusual activity, immediate action can be taken to prevent fraud and unauthorized access.

- How can banks improve the digital banking experience?

The evolution of technology and increasing competition is compelling banks to take steps for a transformed customer experience. This results in customer loyalty, which is a major success factor for banks. Some ways banks are improving their digital banking platforms to achieve customer satisfaction are:

- Simple onboarding process: Deployment of cutting-edge technology to facilitate easy onboarding is emerging as a way to increase adoption of digital banking. By providing self-service options for onboarding, offering new products and services to new customers, and giving the option to access the account through mobile applications are ways the digital banking experience is being improved.

- Utilizing analytics: Big data analytics enable banks to gain an in-depth understanding of the customers so that personalized offerings can be designed. Data helps to create a personalized outreach strategy for different customer categories to provide services pertinent to their unique needs.

- Automation of customer support: To serve customers effectively, banks will need to go beyond traditional customer support to chatbots, customer relationship management and the automation of critical workflows. Repetitive customer queries can be resolved through automation to save time and resources.

- What are the main advantages of digital banking?

The major advantages of digital banking in India are:

- Ease of signing up

- Option to go cash-free

- Convenient use

- Lower fees

- Anytime, anywhere banking

- Personalized offerings and features