In a nation like India, where availing credit is a major contributor to addressing the populace’s financial requirements, requisite processes need to be regulated and monitored to ensure compliance and hassle-free resolutions. With a greater need for credit and lower interest rates, the demand for retail loans is sure to show upward trends in the near future. Therefore, before asking for loan approval, borrowers must be aware of the following fundamental query: Is their credit score meeting the required standard?

Credit scoring in India plays a crucial role in determining loan approvals, and organizations like Equifax, Experian, CRIF High Mark, and CIBIL are engaged in analyzing credit scores to meet the high volume of loans required by retail consumers. Among them, CIBIL, known as TransUnion CIBIL Ltd., is India’s leading credit information company. Established in 2000, it keeps track of loan and credit card payments made by borrowers, making it a key player in the credit ecosystem.

The Credit Information Companies (Regulation) Act, 2005 regulates the CIBIL bureau, which holds a license from the Reserve Bank of India (RBI). Each month, lending organizations such as banks and NBFCs submit the credit histories of their customers to CIBIL. This information is then used to compute the individual’s credit score, which forms the basis for determining his / her creditworthiness, propensity, and eligibility for future credit needs. The database for which CIBIL maintains these records is close to 550 million individual customers and businesses.

What is a credit score?

As per a report, retail loans in India grew by 122 per cent by volume between FY 2021 and FY 2022 – a trend that is likely to continue in 2023. In addition, the personal loan market in India is expected to grow by 10% by 2025. Given this surge, the importance of credit scores will also become greater. People who approach banks and other non-banking lending institutions for retail loans are frequently denied loans and credit cards if their credit score is low. This is partly because many people are unaware of the concept of the CIBIL score and how it can impact their eligibility for credit from their lenders.

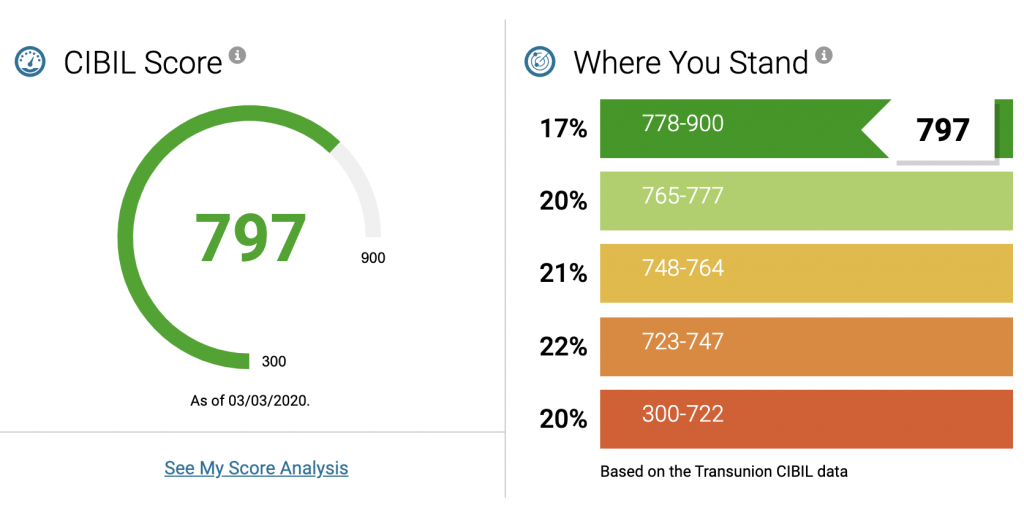

Put simply, a credit score or CIBIL Transunion score is a 3-digit number between 300 and 900 that represents an individual’s credit history. Several parameters are at play to arrive at this numerical figure. A borrower’s chance of getting a loan from a bank or NBFC increases if their credit score is close to 900. A low score indicates bad credit history and makes it more difficult to get a loan approval.

Credit score has changed from being a concept that was previously thought to be outside of the control of borrowers to one that is now available for self-evaluation. The credit score, which is the initial stage of screening and a key factor in determining rejection or approval for credit eligibility, helps to ascertain the applicant’s or borrower’s financial capacity and past behavior. According to a report, self-monitoring borrowers in India have an average CIBIL score of 740 and access their credit reports about six times a year.

The components determining the credit score

Before reaching out to a lending institution, a borrower may self-assess based on the following vital parameters to gauge whether or not they fulfill the essential eligibility criteria:

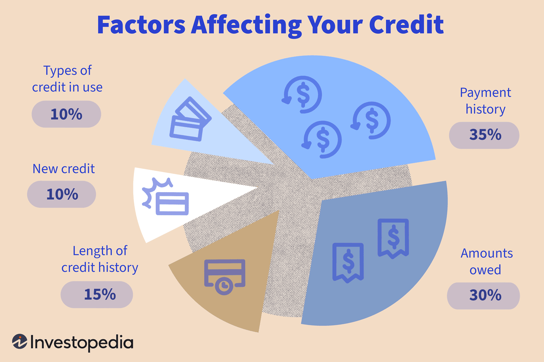

- The total amount of debt: At any given point in time, the total amount of debt will have a major impact on the borrower’s creditworthiness. The credit utilization ratio is the volume of credit availed by the borrower in proportion to the combined credit limit. This ratio should ideally be low to get a high credit score. This would imply that the borrower has availed only part of the credit limit they are eligible for. A healthy credit utilization ratio likely to have a favorable outcome is 30%.

- Payment history: A borrower’s payment history is essential in determining the credit score. Paying loan and credit card dues on time is instrumental in determining the applicant’s propensity to pay future repayments. Late payments of bills affect the credit score, and 30-day delinquency can reduce it by up to 100 points.

- Length of credit: A long credit history shows that the applicant is financially stable enough to handle credit. Lending institutions prefer providing credit to borrowers with a rich credit history because it eases the process of assessing such borrowers.

- Type of credit: It is important to have a decent mix of credit, consisting of a healthy balance of secured and unsecured credit. This helps boost the credit score and lends stability to the borrower’s application.

- Making credit inquiries: Avoiding multiple inquiries in a short period about the credit score also influences the final credit report. Whenever an inquiry is made, the lender pulls out the CIBIL report. This ‘hard inquiry” negatively affects the credit score. On the other hand, a ‘soft enquiry’ is when the borrower checks their score, which can be done multiple times since soft enquiries are not recorded on the report.

The benefits of a good credit score

A good credit score has multiple benefits. Some of these are:

- Easier sanctioning of loans: Since the credit score gives an insight into the creditworthiness of the applicant, it forms the preliminary step in getting a loan sanctioned. A good credit score will aid the approval of the loan, while a low score will lead to rejection. After being satisfied with the credit score, the lender proceeds with the rest of the documentation required for approval of the loan.

- Lower interest rates: A good credit score enables the borrower to choose from several lenders. Based on the interest rates provided by the potential lender, the applicant can make a decision. This is pertinent in car and home loans, where interest rates differ across many lenders.

- Faster disbursements of loans: Banks and lending institutions process the applications faster for those applicants who have a decent credit score. It makes way for faster documentation, processing, and approval.

It is safe to say that credit scores will play a bigger role in the lending landscape as a result of the increase in loan applications and the growing need for liquidity. A good credit score determines not only the approval or rejection of an application but also the rate of interest and the amount of the loan that the borrower is eligible for. Making prompt repayments and considering the aforementioned elements as you work to build financial stability will ensure a better credit profile and more options and opportunities for borrowing.

Recommended Read: The importance of credit risk management

FAQs related to CIBIL score or credit score

- What factors can reduce the credit score?

A borrower’s credit repayment history has the greatest impact on the CIBIL score. Additionally, defaulting or delaying repayments beyond the stipulated time negatively impacts the borrower. As per a CIBIL analysis, a 30-day delinquency can reduce the credit score by up to 100 points.

- Does my bank balance impact the credit score?

The amount in a person’s savings or current account is not reflected in their credit report, nor does it have an impact on their CIBIL score.

- What are the factors on which the CIBIL score depends?

The CIBIL score depends upon factors such as debt-income ratio, previous credit behavior, repayment history, nature of existing loans, length of credit history, credit cards used in the past, credit utilization ratio, or having any outstanding debt. All these factors not only affect the approval of the loan application but also have an impact on the interest rate and the amount of the sanctioned loan.

- How to check my credit score?

Go to the CIBIL website, click on the ‘Know Your Score’ tab, and fill out a form that requires personal information such as an email address, name, date of birth, income proof, and details of previous loans. The applicant’s credit score will be emailed to them after they pay a fee.

- How can credit scores be improved?

In large part, the credit score is impacted by the repayment history and past defaults, if any. Paying dues on time is key. To facilitate this, borrowers must allow automated payment deductions so that there is no room for default, even if they have forgotten the payment date. Besides, credit should be used prudently. Borrowers who take out loans too frequently have weaker credit histories and are more indebted than they should be.