A young population contributing to the e-commerce boom, the rise in digital adoption, and consistent growth in GDP over the past few years, have reinforced Indonesia’s position as a prominent economy in Southeast Asia. Despite many economies facing economic slowdown and yet to recover from the after effects of the pandemic, the Indonesian economy has continued to grow steadily. A larger part of the populace is joining the consumer class with spending power, urbanization and internet penetration continuing to show upward trends. The combination of finance and technology is giving rise to innovation and digital transformation in traditional business models. Given the optimistic forecasts of rising CAGR¹, FinTech in Indonesia have been able to strengthen their foothold. Tapping into this digitization potential with agility, FinTech businesses have been able to grow awareness for FinTechs, which is likely to further aid economic growth.

FinTech in Indonesia: Awareness and the need for inclusion

The Financial Services Authority of Indonesia (OJK or Otoritas Jasa Keuangan) and other agencies have organized seminars, workshops and large events to increase awareness, spread financial literacy and provide easier access to new developments. Financial regulators, investors, students, entrepreneurs and startup founders gather at such events to share knowledge and discuss future possibilities. With support of the Central Bank of Indonesia, OJK has implemented a FinTech registration system for startups. This has legitimized the process and become a step in the right direction for a wider acceptance of FinTech services in Indonesia.

Aside from the economic growth, Indonesia continues to be one of the countries with the highest unbanked population in the world. Per a report, as high as 90 million people in the country do not have a bank account, and another 45 million have little or no access to credit due to deficient credit history or other requisite documentation. The vast and scattered landscape of the country poses several infrastructural roadblocks in implementing the government’s financial agenda. Against this backdrop, the government is pushing for faster financial inclusion through promoting new FinTech entrants and opening up opportunities for entities with the conventional financial model.

Source: Indonesia Investments

The present FinTech scenario and regulatory canvas

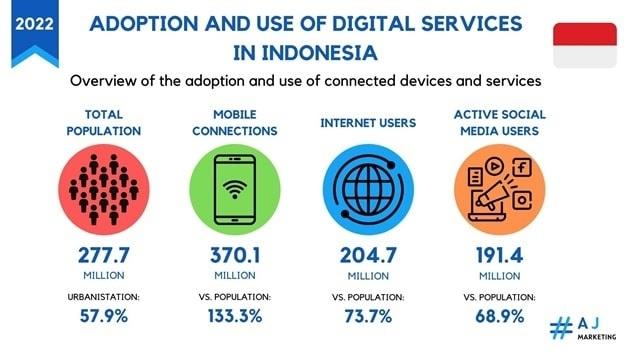

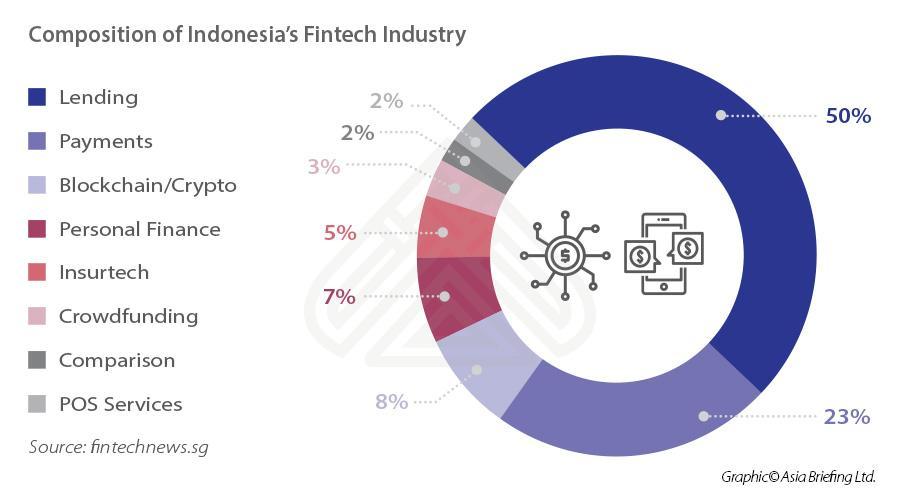

One of the critical drivers for the explosion of digital finance offerings in Indonesia is massive smartphone penetration, estimated to reach 82.84% by the end of 2023. Consequently, internet consumption shows a simultaneous increase. As one of the fastest-growing internet economies in the SEA region, Indonesia is well-positioned to cross the $130 billion mark by 2025². Food delivery apps, e-commerce platforms and app-based local transport services are finding greater interest among the Indonesian population. Within the Indonesian FinTech sector, digital wallets attract the maximum traction presently, followed by P2P lending and B2B FinTech. Global investments in the FinTech sector are also on the rise, successfully generating large amounts of money to create more innovative FinTech products and services.

Businesses in the FinTech sector fall under one of the three regulatory bodies- Bank Indonesia (BI), OJK, or Bappebti – a supervisory authority for commodity trading. While BI regulates payment-related activities, regulations pertaining to cryptocurrency, virtual currency and digital assets fall under the purview of Bappebti. All other segments, including lending and insurance, are regulated by OJK.

Since 2020, regulatory bodies in Indonesia have taken measures to push digitization by working around four key aspects- innovation sandboxes, interoperability, policy framework, and standardization. For example, to drive interoperability, Bank Indonesia capped payment fees on the use of QR codes. Trading is permitted only after approval from Bappebti, subject to multiple conditions. It is important to note that financial transactions and payments through virtual currencies and crypto are prohibited in Indonesia. Before granting a complete operational licence, BI and OJK run sandbox experiments, allowing FinTech institutions to test their pilots under relaxed regulatory conditions for one year.

Collaborations between banks and FinTech institutions over the last few years are notable. However, the challenge exists in standardization and interoperability due to the absence of a foundational digital infrastructure, which has failed to create a multiplier effect for financial inclusion. To counter this, efforts are underway by Bank Indonesia to formulate an interconnected API, to offer a unified interface to consumers to access different types of financial services.

Digital lending

Infrastructure and risk management have been one of the main reasons why conventional lending institutions in Indonesia face difficulties in providing credit access to the untapped population and MSMEs. This gap is where fintech lending has proved to be beneficial. Technology facilitates innovative approaches and different business models to match varying risk appetites of lenders with that of borrowers.

With a shift towards innovation and technology-driven solutions to facilitate better access to financing, the creation of a sustainable and conducive fintech lending ecosystem is in the works. Indonesia is entering the ‘third wave’, a term used to describe a more collaborative fintech lending landscape, marked by the self-regulating organization- Asosiasi FinTech Pendanaan Bersama Indonesia (AFPI) becoming the centre of collaboration between businesses and regulatory bodies. The future of the fintech indsutry will be determined by the ability of key stakeholders to bridge their differing perspectives.

Since inception, the country’s financial framework has been focused on achieving economic growth within a tightly regulated market, which limits the control of platforms operating unethically. Owing to a greater inclination towards traditional practices, for several years, banks have steered clear of innovations such as partnering with P2P lending platforms. However, a recognition of the opportunities presented by these platforms is compelling banks to modify this approach. In an attempt to promote alternative funding in a staggered manner, the number of P2P lending platforms recognized and granted licenses has gradually increased to approximately 103 as of January 2022, as per a report.

Digital payments

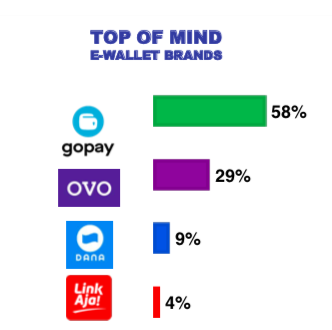

As mentioned earlier, Indonesia is one of the countries with the largest unbanked population. Contrary to India, Indonesia relies heavily on cash and is the second-largest cash-first economy in the world. Credit card penetration³ in Indonesia is the lowest in the region, at just 6%. Thus, digital wallets and e-money have emerged as popular methods for storing and transferring money in the country. Low transaction costs and adoption of digitization are the key drivers behind this surge. To enable a unified payment platform for all transactions across multiple e-wallet providers, the Central Bank of Indonesia has mandated that mobile payment service providers replace QR codes with QRIS (Indonesian Standard QR code). GoPay, DANA, OVO and LinkAja are the top four e-wallet platforms in the country.

Source: KrASIA

The encouraging future of FinTech in Indonesia

With investments coming from various parts of the world, Indonesia is well on its way to become a major financial player in the global economy in the future. Owing to a young population eager to adopt digitization, the government is overcoming the barriers to innovation, which can inhibit growth and limit the accessibility of financial services. Besides, companies looking to transform businesses will need to automate operations in order to enhance productivity and yield. The confluence of these factors, and the tremendous scope for leveraging technology in the finance ecosystem will ensure that FinTech in Indonesia reaches new heights.

FAQs:

- What are the dominant providers of digital financial services in Indonesia?

There is a presence of four key platforms providing digital financial services in Indonesia. These are GoPat, OVO, DANA and LinkAja. These platforms also provide e-money service, and are the most popular in the Indonesian market.

- How many digital banks are there in Indonesia?

20% of the world’s digital banks are in APAC, with Indonesia being home to seven of these. Several more are awaiting licences. This makes Indonesia one of the most potential and promising economies in the SEA region and the world. The rollout of new guidelines for digital banks in 2021 has reduced red-tapism in the market and made it possible for new entrants to grow and penetrate the financial services sector.

- Which country has the highest FinTech adoption?

The largest FinTech market in the world is presently India, with market size estimated to reach $150 bn by 2025.

- Which are the financial regulatory bodies in Indonesia?

In the banking and finance sector, there are three major regulatory entities in Indonesia. Bank Indonesia regulates payment related business activities, while cryptocurrency and digital assets fall under the purview of Bappebti. OJK (Otoritas Jasa Keuangan or Financial Services Authority of Indonesia) controls all activities pertaining to lending, insurance, and all other segments that do not fall under any of the above two categories.

References:

- https://www.statista.com/statistics/1341899/indonesia-retail-market-sales-cagr/

- Gomedici: Indonesia FinTech report 2021

- Xendit: Credit card payments in Indonesia